Unemployment and under-employment

It is expected that the community responses being undertaken to slow the spread of COVID-19 will initially have a primary impact on travel and tourism, and a secondary impact on casual workers in retail trade, accommodation and food services, education and recreational services industries. Collectively, these secondary impact industries make up 45% of the total casual workforce, or approximately 1.1m Australian workers. This group skews in age, with concentrations in the young (>50% of workers under 24) and older (~35% of 65+) demographics1. A second wave could emerge if the crisis is prolonged – impacting full-time professionals in industries such as finance, construction and professional services.

As a credit manager, treatment strategies for both groups will differ significantly. For younger casual-employed borrowers, the lending profile will skew towards lower-exposure unsecured facilities (buy now pay later, credit cards, personal loans) while for the potential second wave of full-time professionals, a greater volume of mortgage facilities will be under stress. For this latter group, there may be the double impact of both increased probability of default as well as potentially elevated loss given default (though it is acknowledged that most lenders real property portfolios currently enjoy significant LVR headroom to absorb a reasonable decline in property values).

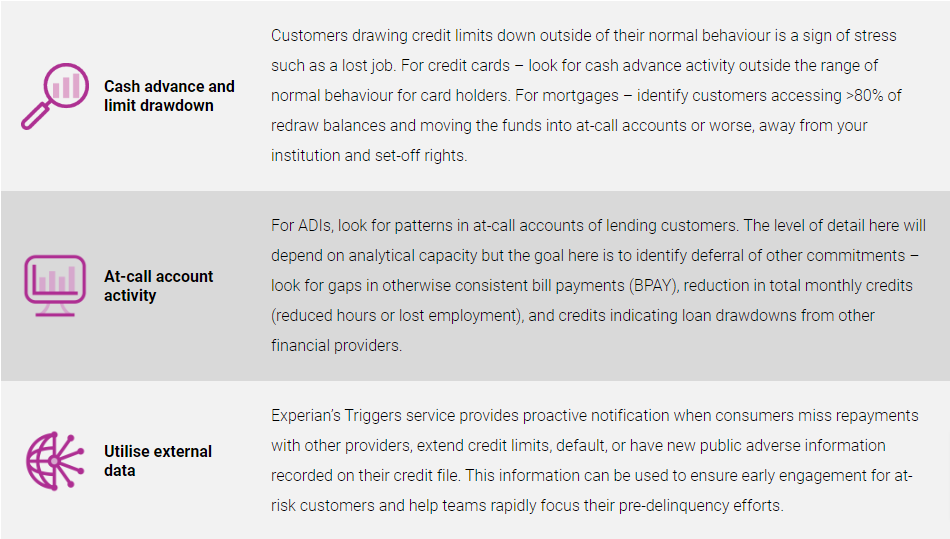

The lenders who take steps to shorten their emergence period will perform best in this period. Identifying the following transactional ‘tells’ will allow lenders to identify at risk borrowers well ahead of their payment default event:

Manage

- For consumers experiencing reduced income – early engagement will, at a minimum, allow for timely intervention and debt management such as restructures, loan holidays or payment deferral. At best, engagement will assist you in moving your facility higher in the consumers payment hierarchy.

- For consumers with total loss of income – early identification will allow hardship program support to commence in a timely manner, to the benefit of both consumers and credit providers.

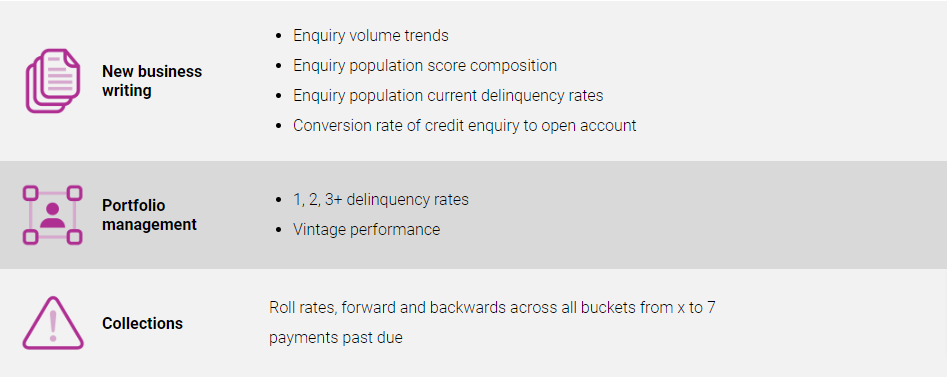

Portfolio management

We are moving into a period where ‘past performance is not a reliable indicator of future performance’. The potential exists for the current uncertain macro-economic factors to buffet retail credit portfolios, driving delinquency up across all lending vintages. Scorecard performance will temporarily deteriorate in this time due to novel (from score development perspective) external factors.

It’s important for credit managers to contextualise performance changes and ensure the classic ‘over-correction’ response is avoided to a spike in bad debts. Over-tightening of new business writing appetite will exacerbate performance metrics measured against book size such as delinquency and loss rates. Further – this type of response typically results in business being declined which would otherwise fit the organisation’s lending appetite.

Comparing portfolio performance to the wider market trend will become a more useful measuring point than comparison to your own historic performance. Experian Horizon is one such tool available in market to enable this. Horizon will allow you to understand contextual performance across the following dimensions:

All of these metrics can be compared against the total market as well as cohorts of your peers. All metrics can also be filtered by product, state, and age profile to allow for more granular insights. This service is provided via hosted web-based tableau instance and for bureau members the product can be available within 10 days. No technical integration work or IT work effort is required.

Continuing to meet analytical requirements

Day-to-day analytics requirements are also likely to increase and there is a strong correlation between rising delinquency rates and rising analytical work in credit risk teams. With many organisations moving to remote working for their workforce for the foreseeable future, the ability to conduct large scale analytics will likely be challenged by VPNs, overloaded internal network infrastructure and limited access to hosted and scalable computational power. Experian’s Ascend platform is a cloud-hosted analytical platform which sits outside of your organisation’s VPNs and is designed from the ground up to be accessed anywhere anytime by its users. Ascend supports a wide variety of analytical tools and is rapidly scalable in both memory and compute power – allowing you to ensure your teams remain highly productive during any period of disruption.

Like our Horizon tool, Ascend can be deployed rapidly for your business and each solution is tailored to suit your teams needs and maximise productivity. Specialist Experian consultants work with your account team to ensure this and will remain available for support ongoing.

Experian is here to help

This is a period of uncertainty for all individuals and businesses. Experian is here to support our partners wherever possible, and is uniquely placed to provide key insight at both the individual and portfolio level.

For further information on any of the above, please contact your Account Director or member of the Credit Services Client Advisory Team. Alternatively, you can get in touch with us using the form below.

1. All per ABS Characteristics of Employment dataset 6333.0