The impact of credit attributes on risk models

Credit attributes have existed for centuries. In days gone by, lenders would make credit decisions based on simple attributes such as employment and income. Although the technology involved with lending has radically changed, with powerful computers and Machine Learning (ML), the theory behind attributes remains the same.

In their simplest form, attributes represent a description of the relationship between different data points that can be used to assess credit risk. Each individual data point provides a limited amount of information on credit behaviour but not the full story – for that bigger picture – they need to be aggregated and combined.

Today, attributes are highly complex mathematical descriptions that combine key data points as ratios over time. These attributes can be used in the development of ML-powered credit risk models to improve the precision of lending decisions. They can also be used without the need for new models to improve score overlays, customer segmentation and marketing pre-screening criteria.

This article answers key questions about credit attributes in a simple and understandable way. Although the details of attribute engineering are extremely technical, our aim is to make the concepts behind them readily accessible across all business units.

Download our attribute PDF - Precision Decisions: Unlocking the value of attributes

DownloadWhat are credit attributes?

Credit bureau attributes represent the relationship between data points that are used to describe the financial characteristics of a borrower. They provide greater insight into credit behaviour than a standard credit score. How? By aggregating and combining individual data points, like credit utilisation and balances, into time-based ratios, such as a debt-to-income ratio over 24 months. Attributes can be used for new model development and as overlays to improve customer segmentation, scores, cut-offs and policy rules.

How do credit attributes improve the accuracy of lending decisions?

Credit attributes enhance the accuracy of lending decisions by providing a more comprehensive understanding of a borrower’s financial situation. This goes beyond a basic credit score as it includes factors like financial stability over time and debt management history to paint a more detailed overall picture.

Credit attributes feed into the credit risk models that assess the likelihood of a borrower repaying a loan or defaulting. By identifying and using the attributes that have the biggest impact on predictability, these models can become significantly more accurate.

Can credit attributes be used without developing new credit risk models?

Yes, attributes can be extremely useful to lenders without the need to develop entirely new models. Attributes can be used as a model overlay to improve segmentation precision – classifying borrowers into different risk categories – which allows lenders to tailor interest rates, credit limits and many other actions for each segment.

Using attributes in this way means lenders can take advantage of attributes without needing a complete model rebuild. Delivering faster, more cost-effective results that can provide meaningful improvements to predictability and thus profitability.

What are trended attributes?

Trended attributes analyse a borrower’s behaviour over a given time period to provide a dynamic view of their financial situation. They track key data points, such as loan balances and repayment amounts, to reveal trends that would not otherwise be apparent. These trends give lenders a more nuanced view than a fixed-time snapshot.

When trended attributes are incorporated into a credit scoring model, they improve the accuracy of the assessment by showing the borrower’s financial trajectory. Historical payment trends, such as credit utilisation ratio (credit usage vs. credit availability), provide a better overview of a borrower’s financial situation by identifying if their payment capacity is improving or deteriorating.

How are credit attributes created?

Attributes are created by analysing, aggregating and combining credit data points to identify hidden relationships or patterns in credit behaviour. Each attribute is carefully derived from a huge amount of raw data due to its ability to impact the predictability of the final risk model.

Depending on the size and resources available to the financial institute, they may develop their attributes in-house or source them from credit bureaus. In many cases, lenders work closely with experts from bureaus to identify the most relevant, reliable and predictive attributes for their specific type of lending and market.

Why is it challenging to identify the best attributes?

Just because an attribute exists does not mean that it will improve the accuracy of a credit risk model. In fact, using too many attributes can have the opposite effect and reduce the accuracy of a model. The key is the relevance and the impact on predictiveness of the attribute. Identifying the most relevant attributes for a model is a highly specialised task.

Additional challenges in attribute selection include:

- Data availability – does the lender have access to the necessary raw data?

- Data quality – the accuracy and reliability of the data used to develop attributes is critical to their success, bias or inaccuracies lead to flawed attributes.

- Data aggregation – individual data points can easily amount to hundreds of millions across a portfolio, so aggregation is critical to attribute development.

Download our attribute PDF - Precision Decisions: Unlocking the value of attributes

Download

Download our attribute PDF - Precision Decisions: Unlocking the value of attributes

DownloadDoes Machine Learning (ML) enhance credit attribute accuracy?

Yes, ML can play a significant role in enhancing credit attribute development by revealing non-linear correlations between data points. ML algorithms can identify complex relationships between multiple data points that may have otherwise been missed.

This can result in attributes that have a stronger predictive power. ML can also be used to create new model features by combining multiple attributes.

How to choose the best attributes for a credit risk model?

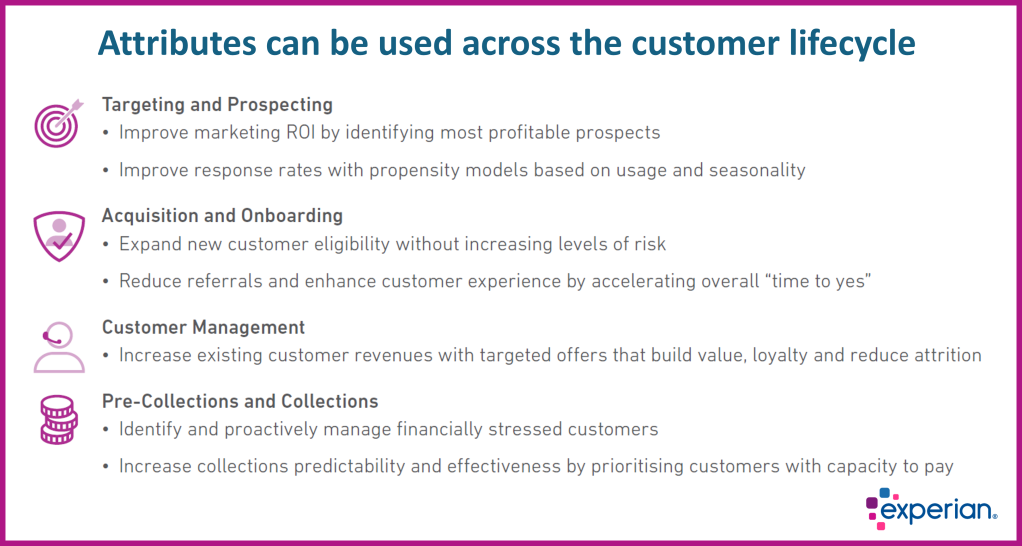

Attribute selection depends on the type of lending, the stage of the customer lifecycle and the sector. Experian has a library of thousands of attributes – including a core subset of the most widely used attributes and additional subsets for different industries.

The best attributes to use are those that have the greatest impact on the predictive accuracy of a risk model. Assessing the impact of each attribute and then assigning it a weight within the final model is a complex process.

Do credit attributes need to change over time?

Yes, credit attributes absolutely need to change and evolve over time to retain high levels of predictive accuracy in credit risk assessment. This is due to the constantly changing macroeconomic environment and the resulting shifts in borrower behaviour.

The last few years have seen considerable changes in many consumers’ financial situations due to elevated inflation and interest rates. For younger borrowers, this represents their first cycle of raised interest rates, so attributes that were previously highly predictive may need to be updated to remain relevant.

Trended attributes – that can include data points over a two-year period – are particularly important in light of the rapid changes in interest rates that many regions across the world are experiencing at the moment.

How do attributes contribute to automated credit decisioning?

Attributes play a crucial role in optimising the automation of credit decisions. The right attributes can significantly improve the accuracy and reliability of the models that power lending software. The end result is that businesses can trust that their automated credit assessments are consistent, inclusive and responsible.

Download our attribute PDF - Precision Decisions: Unlocking the value of attributes

Download

Download our attribute PDF - Precision Decisions: Unlocking the value of attributes

DownloadAre you interested in using the latest attributes in your decision engine?

If you’d like to boost the accuracy of your credit decisions with the latest and most predictive attributes, then speak to your local Experian representative today. You can benefit from our many decades of experience developing and integrating attributes for use across the consumer credit lifecycle. Using our attributes can deliver as much as a 20% increase in the Gini coefficient predictiveness of a model.

For more information about Experian’s attributes, download our Precision Decisions: Unlocking the value of attributes PDF guide.