Research published in Experian’s 2022 Business and Consumer Insight Report found that around half of consumers recognise that, if they want access to a product or service, their data must be shared. For example, almost one in two consumers are willing to grant companies access to their financial information to receive help with online application checks for financial products.

Consumers’ willingness to share data unlocks opportunities for businesses. Data can be turned into actionable insights that enable companies to improve their performance and provide a better and more personalised customer experience. In turn, enhanced customer experience is likely to further encourage consumers to share data.

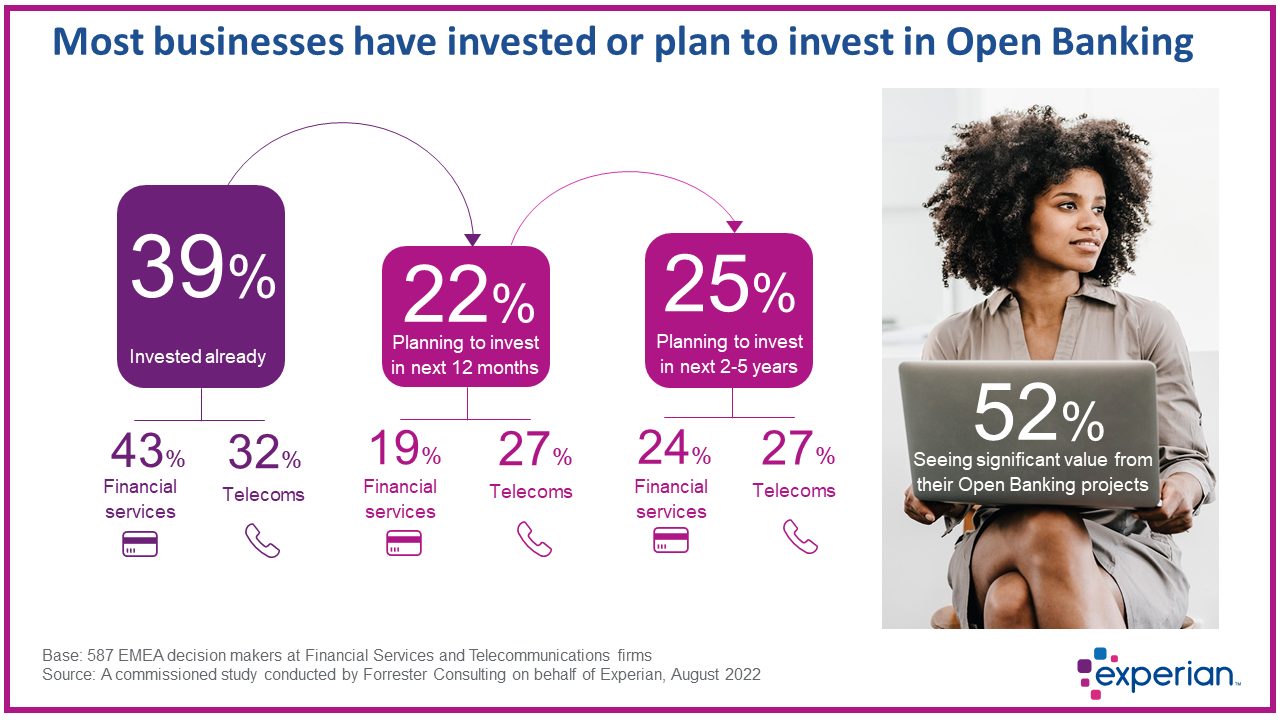

This is the virtuous circle of Open Banking. And the promise of a better customer experience is boosting Financial Services and Telecom providers’ investments in Open Banking. This is clearly illustrated by the fact that 86% of the business respondents have already invested or are planning to invest in Open Banking, and more than half (52%) are seeing significant value from their Open Banking projects.

Consumer consent is key

For those businesses the value of Open Banking is clear. However, many consumers are yet to fully understand the value and benefits that it can provide. Businesses need to clearly articulate this value exchange to potential customers to encourage those consumers that are still hesitant to share their data.

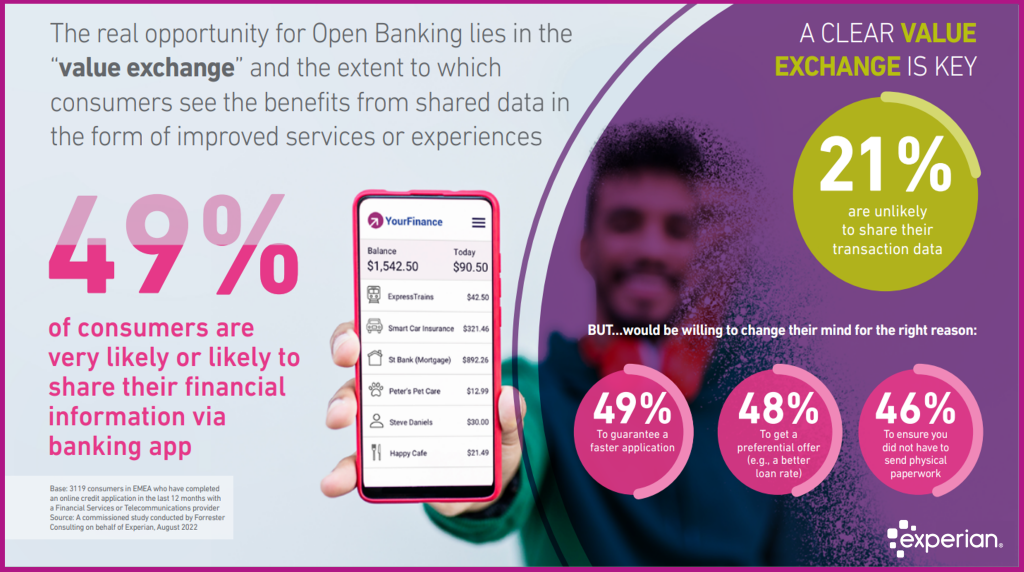

Experian’s research indicates that 21% of consumers are unlikely to share their data, but a significant proportion of this same group would be willing to change their minds for the right reason. Explaining the advantages of sharing their data via Open Banking at the point of consent in the application process is vital for businesses to avoid losing these potential consumers.

Nearly half of the surveyed consumers who were unlikely to share their data were willing to do so if it guaranteed a faster application process. 48% were willing if it would give them a preferential offer, such as a better loan rate, and 46% to ensure that they would not have to submit any paperwork. By including these benefits in the application process businesses can improve the speed of lending decisions and take advantage of the increased depth of data available from consumer-consented financial information.

Augmenting bureau-based scores with transactional data

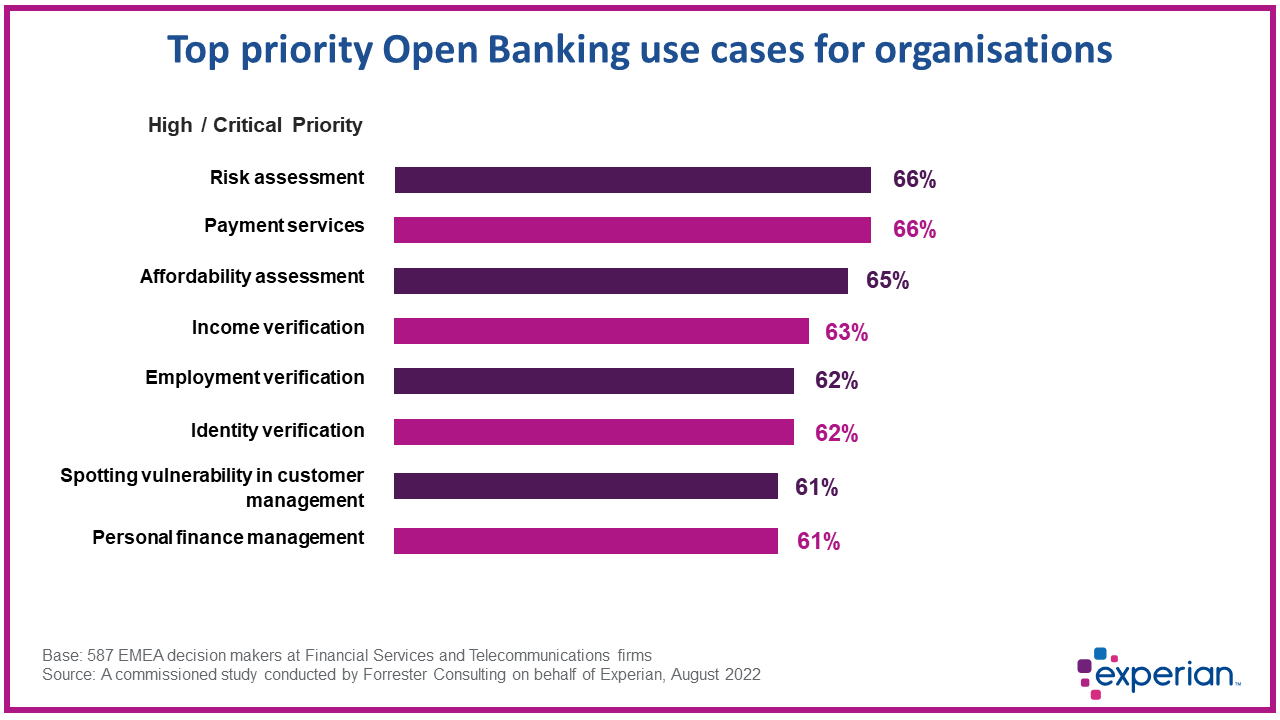

Businesses are leveraging Open Banking across a wide range of use cases to improve multiple aspects of their operations. One of the top priority use cases is that of risk assessment. This was highlighted by 66% of the Financial Services and Telecoms firms surveyed in Experian’s latest research.

This is where transactional data from Open Banking can be especially powerful. Instead of relying on a bureau-based score to access the creditworthiness or affordability of a potential customer, businesses can now use transactional data from Open Banking to develop their own standalone risk assessment score. By combining data sources businesses can build a much stronger risk assessment model than is possible with only a bureau-based score. Transactional data provides detailed insight into each customer and is extremely valuable in assessing risk throughout the customer life cycle.

Another relevant point to emerge from the research is the wide range of critical and high priority use cases applicable to Open Banking. The variety of use cases highlighted by businesses is striking. As well as risk assessment these include payments services, affordability assessments, income, employment and identity verification, spotting customer vulnerability and personal financial management.

The journey towards Open Data

Open Banking is far from being the ultimate destination. It can be seen as a steppingstone on the way to creating an economic system based on Open Data – where consented account data is connected from sectors other than finance, including insurance, telecoms, energy and even government held data.

In this “new world”, data will be transferred effortlessly post-consent and information will flow in near real-time. It will mark the departure from the “old world” of manual customer steps. For instance, it will make printing and sending documents – one of the main causes of application abandonment – a thing of the past.

Not only will Open Data allow businesses to abandon many traditional, manual, practices. It will also lead to a considerable reduction in the number of steps that still slow down digital processes, such as downloading a payslip from a portal and uploading it to another, in the case of a mortgage application.

This is a big deal for Financial Services and Telecoms businesses, which have long struggled to match the online customer experience offered in other sectors, due to the number of procedures and checks necessary to satisfy regulatory requirements. Open Data will finally allow them to address this point effectively, enabling Financial Services and Telecoms businesses to enhance the overall digital experience provided and streamline the support available to customers.

For instance, personal identity and financial documents could be held in a digital identity wallet, owned and managed by the consumer. When applying for a loan, the customer would select the documents required for the specific application they are submitting, for instance, a driving license for identification and bank transaction information to demonstrate affordability, and these will be securely shared with the lender to complete the application process. The speed at which consumers can apply and businesses can run financial checks will be shortened considerably.

It is no exaggeration to say that we are entering a new era of business services. The shift to Open Data will enable Financial Services and Telecoms businesses to exceed customer expectations and interact with unprecedented levels of convenience and simplicity.

While these benefits are glaringly apparent to businesses, it’s crucial that they clearly articulate the advantages to potential customers. Familiarity with Open Banking is growing fast and those businesses that help to educate the public stand to be at an advantage over their competition.

For more detailed insight into consumer and business attitudes toward Open Banking, download Experian’s latest report.