A growing number of online businesses are choosing to provide Buy-Now-Pay-Later (BNPL) services to improve their customer experience and increase conversion rates. When you consider that 78% of global consumers say their opinion of a brand improves when it offers BNPL at checkout, it’s clear that this payment option has become an essential part of the eCommerce payment landscape.

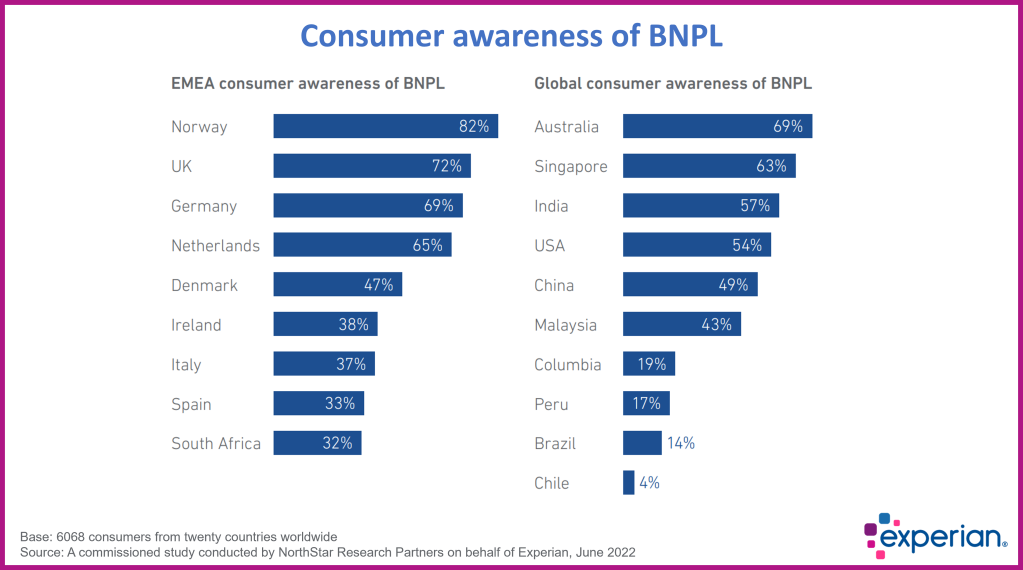

According to Experian’s research of over 3000 consumers, 3 in 4 of the respondents have used BNPL in the last year, with 11% using BNPL weekly to make purchases. This illustrates how widespread and popular this alternative payment method has become. But the meteoric rise of BNPL has also attracted the attention of fraudsters.

At the core of BNPL is the speed and ease with which consumers can access credit, yet these very attributes make it susceptible to fraud. This article looks at the problem of BNPL fraud and how BNPL providers can use cutting-edge technology to reduce their fraud losses while still providing a fast and convenient service to merchants.

Why is fraud a problem for BNPL?

There are three main reasons why BNPL platforms are especially vulnerable to fraud. The first of these is due to the way that BNPL payments are structured. Customers initially pay only a small amount – usually 25% – of the total cost of the goods/service. This makes the platform appealing to fraudsters who can gain access to goods at a fraction of their real value.

BNPL platforms are designed to be as frictionless as possible with a credit decision made in seconds. Compared with a traditional loan or credit card application this process has far fewer identity and creditworthiness authentication steps to complete and rarely includes two-factor authentication. Fraudsters can access customer login credentials through complex phishing attacks and then use these to conduct BNPL fraud.

Many regions are in the process of developing regulations to govern the use of BNPL, however, this may still take years to implement. Without a regulatory framework in place, BNPL providers have to develop their own methods for conducting identity and credit checks. The challenge is to balance a fast and simple checkout process with adequate fraud prevention, which is highly dependent on the accuracy of the fraud solution that each provider uses.

What types of fraud affect BNPL providers?

Most of the fraud cases that impact BNPL providers involve some sort of identity theft. Fraudsters obtain this information either from phishing attacks or by purchasing it off the dark web. It allows them to create synthetic identities – that use components of real data with fake data – to create new BNPL accounts or take over existing accounts.

Let’s take a closer look at some of the other common types of BNPL fraud.

- Account takeover

Compared with the time and effort required to create a synthetic identity it is much easier for a fraudster to take over an existing BNPL account. This allows them to change the delivery address details and make purchases using an established customer’s higher credit limit.

- Buy-Now-Pay-Never

This can happen when a legitimate customer uses their own data or when a fraudster uses stolen data to pass security checks to access goods/services with a BNPL plan. Once the merchant has delivered the product the fraudster vanishes without completing the remaining payments.

- Chargebacks

Whenever a purchase is disputed and directly reported to the customer’s bank the result is usually a chargeback. In some cases this involves legitimate customers that abuse this system with the intention of keeping the product and being reimbursed for it – this is known as “friendly fraud”. However, chargebacks are also a common tactic used by professional fraudsters.

- Return abuse

Most digital merchants offer some kind of return policy and this can be abused by fraudsters who return the item after already using it or returning a completely different item. This type of fraud is difficult to detect as fraudsters often use their own identity and then falsely claim that the item was not delivered, is missing components or is damaged.

BNPL providers that are able to provide their clients with advanced fraud protection will be at an advantage in this increasingly competitive space. Given the unregulated environment, it is essential that merchants ensure that their BNPL provider is using the latest technology to proactively screen customers and mitigate fraud losses.

How can BNPL providers reduce fraud?

The biggest reason why the BNPL model is so successful is that it offers consumers instant access to credit – maintaining this simple point-of-sale loan is an essential element of this payment method. So how can BNPL providers offer a frictionless service while still having the best possible fraud prevention system?

To continue to deliver a fast and secure checkout experience BNPL providers need to make use of new technology to more accurately assess fraud, but in a passive way that does not interfere with the customer experience. In order to do that, businesses are increasingly looking to AI, Machine Learning (ML) and device fingerprinting to unobtrusively screen potential customers in real-time.

The power of Machine Learning

The high-performance analytical power of ML allows BNPL providers to identify fraud far more accurately than using fraud rules alone. ML can make connections between previous fraud cases and new transactions as they happen to proactively identify and prevent fraud.

With ML technology, BNPL providers can analyse transactions in a much more efficient way, not only detecting patterns that would have been missed by legacy systems, but also reducing pressure on internal fraud teams to manually review transactions, as a greater proportion of decisions can be automated.

Another important benefit of ML is that the models can continually retrain to stay at pace with changing fraud threats as they develop. Every fraud case can be added to the model to keep it up to date – and at the cutting edge of fraud trends. Manual review cases can also be added to the model so that it progressively provides more accurate recommendations over time.

Device tracking and verification

Device fingerprinting is another technology that can significantly elevate fraud screening for BNPL providers. It allows them to collect and analyse unique identity data from every device that uses their platform and can greatly enhance their fraud prevention capabilities.

By combining ML with device fingerprinting in a multi-layered approach BNPL providers can analyse customer behaviour and device data in a fraction of a second to identify fraudsters before they make a purchase. This process happens automatically so that legitimate customers are not inconvenienced in any way as they pass straight through to checkout.

ML and device fingerprinting is the best way to analyse device location, operating system, timestamp and other data to identify subtle changes in user behaviour that indicates a fraud risk. By monitoring account logins for new devices, changes in IP address and password resets BNPL providers can flag suspicious behaviour before the fraudster moves onto the payment stage.

Experian’s new AI fraud solution for BNPL providers

As a global leader in fraud prevention software, Experian understands the importance of providing your customers with a frictionless payment journey while maintaining the highest levels of security. Our latest fraud solution – called Aidrian – was designed to help BNPL providers find the perfect balance between customer experience and fraud prevention.

The ML algorithms that power Aidrian use your own data to understand your specific fraud threat and they continually retrain on new data to help you stay at pace as fraud changes. It’s not just the ML model that is customised to your business, every aspect of Aidrian can be customised to provide a solution that’s highly efficient and simple to use. Contact us today to speak to your local consultant and set up a proof-of-concept trial.